Lead generation services for financial advisors tend to get sold in one of two ways.

Either they promise the moon with a suspiciously cheerful smile, or they bury the details under enough jargon to make confusion sound premium.

Neither is helpful.

If you are evaluating a lead generation provider, the real question is not “Can they get me leads?” Almost anyone can get you names. The better question is what kind of opportunities they are actually delivering, how much context you get before outreach, and what success is supposed to look like once those households arrive.

That is where real vetting starts.

Why advisors get burned by lead generation services

A lot of disappointment in lead generation has nothing to do with volume. It has to do with mismatch.

The advisor thinks they are buying warm opportunities. The provider is really selling contact records. The advisor expects conversations. The provider is measuring form fills. The advisor wants consistency. The provider is talking in vague averages and optimistic timelines.

That is why a provider can sound great in a sales conversation and still be a bad fit in practice.

Lead generation is not just a traffic source. It becomes part of your growth system. If the quality is weak, the data is thin, or the expectations are fuzzy, you do not just lose money. You lose time, momentum, and trust in the channel itself.

Start with the contract, not the pitch

A slick demo can hide a lot of unpleasant details.

Before you get too impressed by dashboards, promised volume, or cheerful sales language, look at the commercial structure.

Ask questions like:

- Are you locked into a long term contract?

- Is it month to month?

- Are there minimum commitments?

- Can pricing change by market?

- Is there any guarantee around delivery volume?

- What happens if the quality is poor?

- How easy is it to cancel?

This matters because the contract tells you how much confidence the provider has in its own product.

A strong service should be understandable and reasonably easy to leave if it is not working. If the provider needs a long lock-in before you have even seen whether the fit is real, that is usually worth slowing down for.

Ask what “a lead” actually means

This sounds basic. It is not.

A lot of advisor lead generation problems start with a definition gap. One provider says “lead” and means someone who clicked an ad. Another means someone who filled out a short form. Another means someone who completed a more detailed planning step. Another means a contact record that has been sitting in a database waiting for a second life.

So ask directly:

- What has this person actually done before I receive them?

- Did they request something?

- Did they complete a questionnaire?

- Did they build a plan?

- Did they explicitly agree to be contacted?

- Are they exclusive to me, or sold to multiple advisors?

If the provider cannot answer that cleanly, that is a problem.

The more clearly they can define the action behind the lead, the easier it becomes to judge whether the opportunity is actually worth your time.

Look hard at the data you get before the first call

This is one of the biggest separators between usable lead generation and miserable lead generation.

If the provider gives you almost no context, you are forced to do all the trust-building from zero. That usually means more awkward openings, weaker conversations, and more time wasted figuring out whether the person on the other end is even remotely aligned.

Good questions here are:

- What information do I receive before I call?

- Do I get financial details, goals, or household context?

- Are the phone numbers validated?

- Is the email real?

- Do I know why this household was interested in the first place?

- Can I see anything that helps me tailor the first conversation?

The more context you have, the more relevant your first outreach can be.

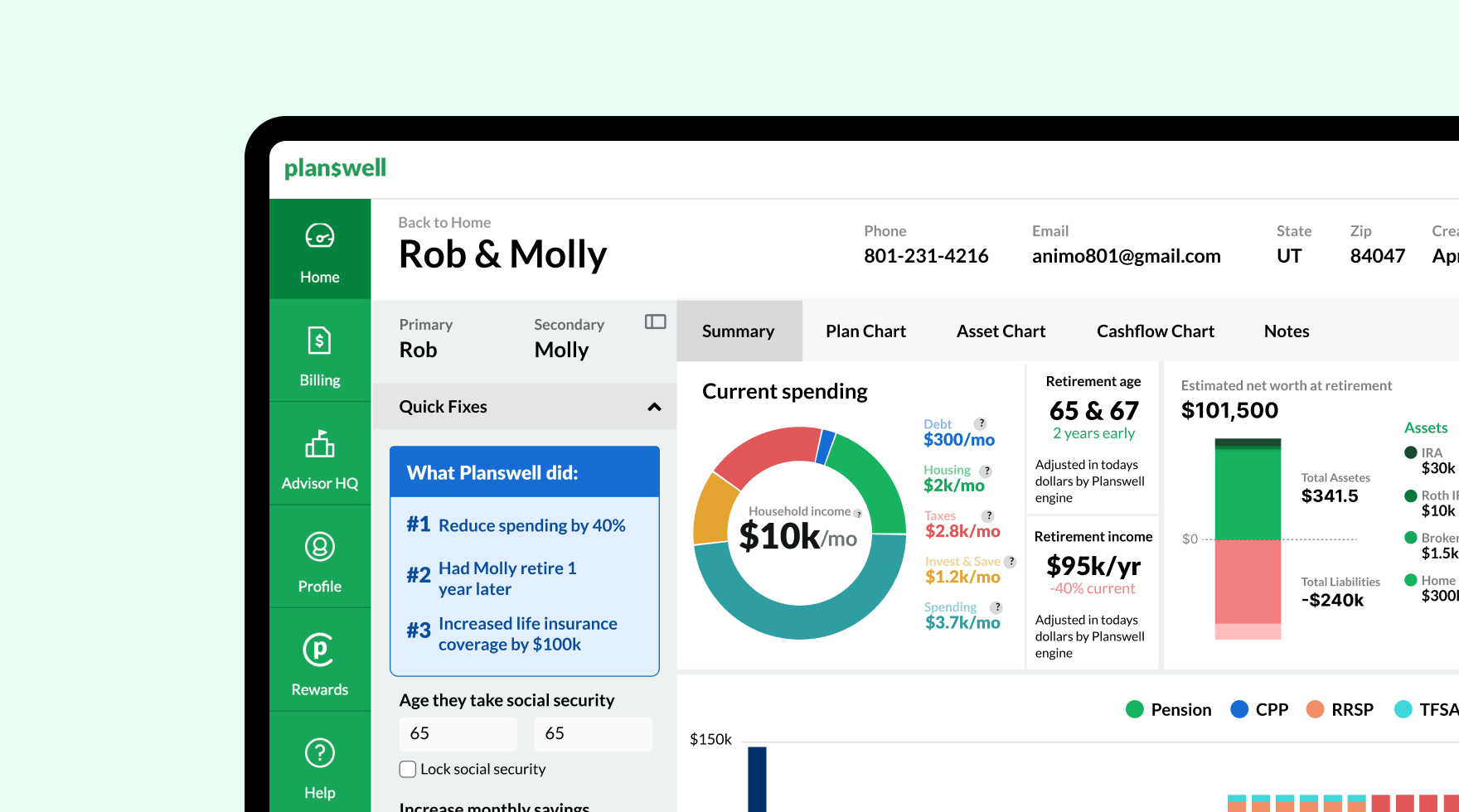

That is one reason we put so much emphasis on household data inside Planswell. A lead source becomes much more useful when the advisor is not starting blind.

Vet the support, not just the lead flow

A lot of providers act like their job ends at delivery.

That is a weak model, especially in financial services, where follow-up speed, scripting, objection handling, and consistency all affect outcomes.

So ask:

- Do they provide onboarding?

- Do they offer training?

- Are there scripts or outreach resources?

- Is there guidance on how to handle first calls?

- Is there anyone you can talk to if results are weak?

- Do they help you improve, or just keep sending names?

This part gets overlooked all the time.

A provider can have decent lead flow and still be a poor growth partner if you are left to invent the entire follow-up system yourself. If there is no support around what happens after delivery, the real cost is higher than it looks.

Ask how exclusivity works

This one matters more than people think.

A “lead” feels very different when you are the only advisor contacting that household versus one of several.

Ask directly:

- Is this opportunity exclusive?

- If yes, what does exclusive actually mean?

- Is the household routed to one advisor only?

- Is there any recycling or resale?

- Do exclusivity rules vary by geography or product tier?

- Are there limits to how exclusivity is defined?

This is one area where it helps to compare providers against a stronger model. With Planswell, for example, advisors receive exclusive household opportunities rather than competing over the same contact with a pack of other advisors. That changes the dynamic quite a bit. Your follow-up still matters, but you are not walking into a race the moment the lead hits your dashboard.

If a provider sells shared leads, that does not automatically make the model bad. But the pricing, expectations, and follow-up urgency should reflect that reality.

You should not be paying premium prices for what is basically a sprint against other people’s outbound.

Be suspicious of unrealistic expectations

This is where a lot of advisors get seduced.

A provider says the leads are “hot.” They imply the pipeline will swell immediately. They talk like the only thing standing between you and explosive growth is signing the agreement and maybe smiling more on calls.

No serious channel works that cleanly.

Even strong lead generation usually still depends on:

- speed to lead

- consistent follow-up

- a decent first call

- a clear next step

- enough repetition for the process to compound

If a provider is talking like the leads should close themselves, that is not confidence. That is sales fog.

A good provider should be able to tell you what they are responsible for and what still depends on you.

Judge the service on clarity, not just cost

Cheaper is not always better. More expensive is definitely not always better.

What you want is clarity.

Can the provider tell you:

- exactly what you are buying

- how many opportunities to expect

- what data comes with them

- whether they are exclusive

- what support exists

- what kind of timeline is realistic

- what happens if things are not working

If too many of those answers come wrapped in vague language, optimistic hedging, or sales choreography, the service probably is not ready to be judged as a serious growth channel.

The point of vetting is not to find the flashiest promise. It is to reduce ambiguity.

What a stronger lead generation model looks like

If you want a useful benchmark, look for a provider that gives advisors more than just names in a spreadsheet.

That means clear terms, strong household data, exclusivity, and support around what happens after the handoff.

That is the model we aim for with Planswell.

We do not just hand over a contact record and wish you luck. Advisors get exclusive household opportunities, meaningful household context, and tools that make follow-up more relevant and more actionable. The point is to make those first conversations feel warmer, clearer, and easier to move forward.

That does not mean every advisor should choose the exact same solution. It means this is the level of clarity and support worth looking for when you compare providers.

A simple checklist for vetting lead generation providers

Before signing with any service, make sure you can answer these clearly:

- What exactly counts as a lead?

- What action did the household take before I receive them?

- Are the opportunities exclusive?

- What data do I get before outreach?

- Are the phone numbers or emails validated?

- Is there a long term contract?

- Is there a guaranteed delivery volume?

- What support comes with the service?

- What does success realistically depend on from my side?

- How quickly should I expect conversations, not just names?

If too many of those answers are vague, the service probably is too.

The mistake advisors make when comparing providers

A lot of advisors compare lead gen services too narrowly.

They look at the sticker price, maybe the promised number of leads, and whether the provider sounds polished in the meeting.

That misses a lot.

The better comparison is total usability.

How much context do you get? How much work do you still have to do? How much guesswork is left on your side? How much support exists once the leads start arriving? How likely is it that the opportunities will translate into actual conversations?

A cheaper service with thin data and no support can be much more expensive in practice than a stronger service with better structure.

Final thought

Lead generation services for financial advisors are not all solving the same problem.

Some sell attention. Some sell contact records. Some sell actual household opportunities. Some sell optimism dressed up as a growth strategy.

The more clearly you can separate those categories, the easier it becomes to buy well.

That is what vetting is really for.

Not to find the company with the slickest pitch. To find the one that gives you the best shot at real conversations, with real context, under terms you can actually live with.