Navigating the complexities of financial advising can be tricky, and even the most seasoned advisors can slip up. Here are the top ten missteps to avoid to ensure you provide stellar service to your clients:

1. Ignoring Spousal Inclusion

Financial planning is very much a team effort, especially for couples with intertwined goals and resources. When advisors focus only on one partner, it can lead to misunderstandings and a plan that doesn’t fully reflect the couple’s joint aspirations. Both partners often bring distinct perspectives and values to the table, making their combined input crucial for crafting a comprehensive financial strategy.

Involving both partners in all discussions ensures that every aspect of the plan respects their shared and individual goals. This approach not only makes the financial advice more effective but also helps both partners feel equally invested and responsible for the outcomes. Additionally, this inclusive strategy enhances communication between the couple and the advisor, building a stronger foundation of trust and cooperation.

Keeping both partners in the loop and actively engaged in the financial planning process also helps prevent potential conflicts about money down the line. It solidifies the advisor's role as a facilitator of their financial health, showcasing commitment to understanding and addressing the needs of both clients equally.

2. Overusing Jargon

When it comes to financial advice, clarity is key. Using too much industry jargon can create barriers, making clients feel out of their depth. A simpler, more direct communication style helps clients understand complex financial concepts and decisions more easily. This approach not only demystifies finance but also empowers clients, making them more confident in their financial choices.

Advisors should focus on breaking down information into digestible, clear terms that all clients can understand. This not only enhances client comprehension but also fosters a more inclusive and supportive advisory environment. Clear communication builds trust and helps clients feel more connected to their financial journey.

3. Neglecting Transparency with Fees

Understanding the cost of services is crucial for clients. A lack of transparency regarding fees can erode trust and discourage clients from fully engaging with their financial plans. Advisors should be upfront about their fees, explaining how they are structured and what clients receive in return. This transparency reinforces the value of the advisor's services and builds a stronger, trust-based relationship.

Open discussions about fees help avoid misunderstandings and ensure clients feel respected and valued. This clarity allows clients to make informed decisions about their financial management, reinforcing their confidence in their advisor's integrity and commitment.

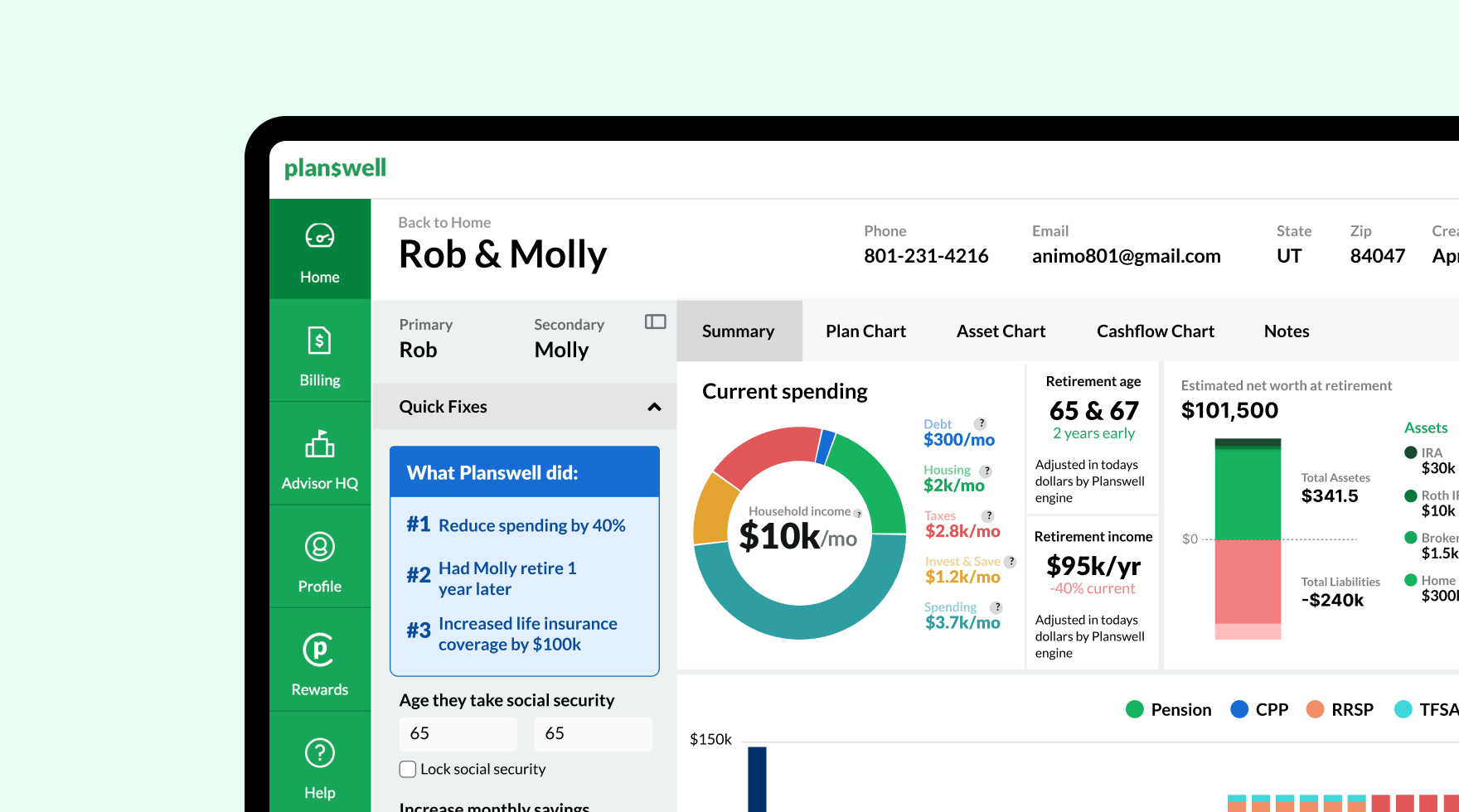

4. Not Tailoring Recommendations

Each client has unique financial situations and goals, which calls for personalized advice tailored to their specific circumstances. Generic advice not only risks missing critical aspects of a client's financial life but also may appear insincere. Advisors should invest time in understanding each client’s personal and financial background to offer customized, relevant guidance.

This personal touch shows clients that their individual needs are recognized and valued, enhancing their trust and satisfaction with the service. Tailored advice is generally more effective, helping clients achieve their specific financial goals while reflecting their personal values and lifestyle.

5. Failing to Follow Up

Consistent follow-up is key to maintaining strong client relationships and adapting strategies to changing circumstances. Without regular check-ins, clients may feel neglected or overlooked, potentially leading them to seek advice elsewhere. Effective follow-up demonstrates an advisor's commitment to their clients' ongoing financial success and well-being.

Scheduled reviews and updates help keep clients engaged and informed about their financial progress. These interactions are opportunities to reassess goals, celebrate achievements, and make necessary adjustments, ensuring that the financial plan remains aligned with the client's current needs and future aspirations.

6. Underestimating Emotional Intelligence

Financial decisions are often deeply personal and can be emotionally driven. Advisors who fail to engage with the emotional aspects of financial planning may struggle to connect with their clients on a meaningful level. Emotional intelligence is crucial for understanding clients' concerns, motivations, and fears.

By acknowledging and addressing the emotional factors involved in financial decisions, advisors can foster deeper relationships and offer more empathetic and supportive guidance. This approach not only improves client satisfaction but also enhances decision-making, leading to more successful financial outcomes.

7. Avoiding Technology

In an increasingly digital world, technology plays a critical role in enhancing advisory services. Advisors who resist incorporating technology into their practices may miss out on efficiencies and client engagement opportunities. Modern tools offer enhanced data management, more effective communication channels, and streamlined processes, improving service delivery.

Embracing technology allows advisors to meet clients' expectations for accessibility and convenience while maintaining high service standards. This not only improves operational efficiency but also enhances the client experience, keeping the practice competitive in a rapidly evolving market.

8. Not Setting Expectations

Setting realistic expectations is essential for client satisfaction and trust. Advisors who overpromise and underdeliver risk damaging their professional relationships and credibility. It’s important for advisors to manage expectations from the start, clearly outlining what can be achieved with the available resources and within the current financial landscape.

Honest and realistic discussions about potential outcomes and risks help clients prepare for various scenarios and foster a trusting advisory relationship. This transparency ensures that clients are not only informed but also more resilient to potential financial setbacks.

9. Poor Risk Management

Effective risk management is fundamental to financial advising. Advisors need to clearly communicate the risks associated with different financial strategies to prevent misunderstandings and potential losses. Comprehensive risk assessment and clear explanations help clients make informed decisions, matching their risk tolerance with suitable strategies.

This thorough approach to risk helps protect clients' assets and ensures long-term satisfaction with their financial strategies. Advisors who excel in risk management not only safeguard their clients' interests but also build their reputation as diligent and trustworthy professionals.

10. Lacking a Holistic Approach

A comprehensive view of a client's financial situation is crucial for effective advising. Focusing on only one aspect, such as investments, without considering other areas like debt management and estate planning, can hinder a client’s overall financial health. Advisors should ensure they address all aspects of financial planning to provide complete and effective guidance.

By considering the full spectrum of financial activities, advisors can offer more integrated and effective strategies that address short and long-term goals. This holistic approach not only enhances the quality of advice but also helps clients achieve a more secure and prosperous financial future.

By steering clear of these common pitfalls, advisors can enhance their credibility, strengthen client relationships, and establish a reputation as trusted and effective professionals. Keep these tips in mind to elevate your practice and deliver outstanding service to your clients.