.png)

Alex tried prospecting with Linkedin and "traditional" lead gen services.

(Watch Time—6:06)

Now that he's tried Planswell, it's safe to say he won't be going back.

When you buy a lead list, all you know about the person you're calling is their phone number. How are you supposed to build rapport in that situation?

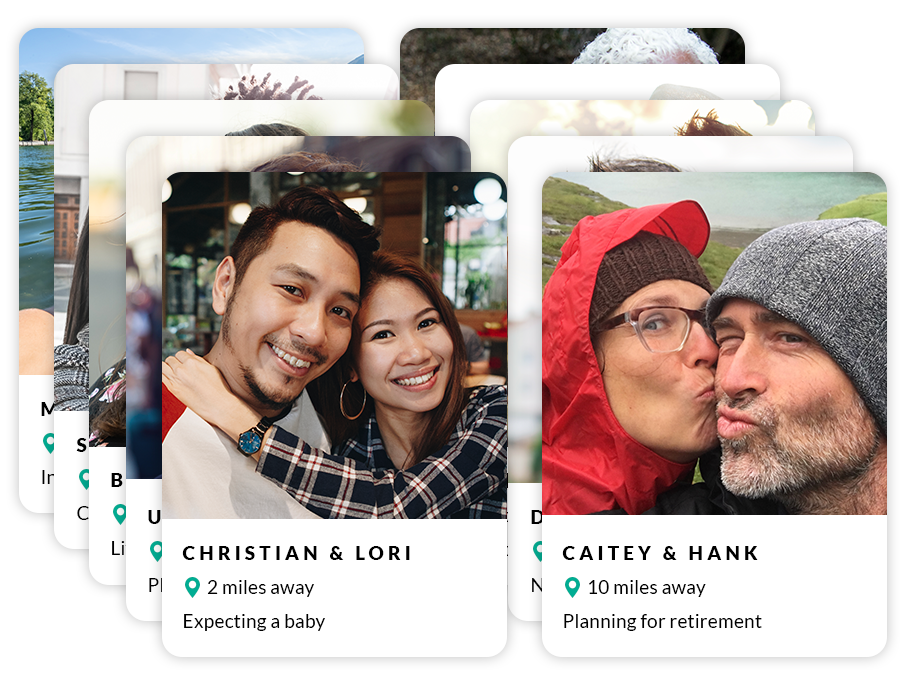

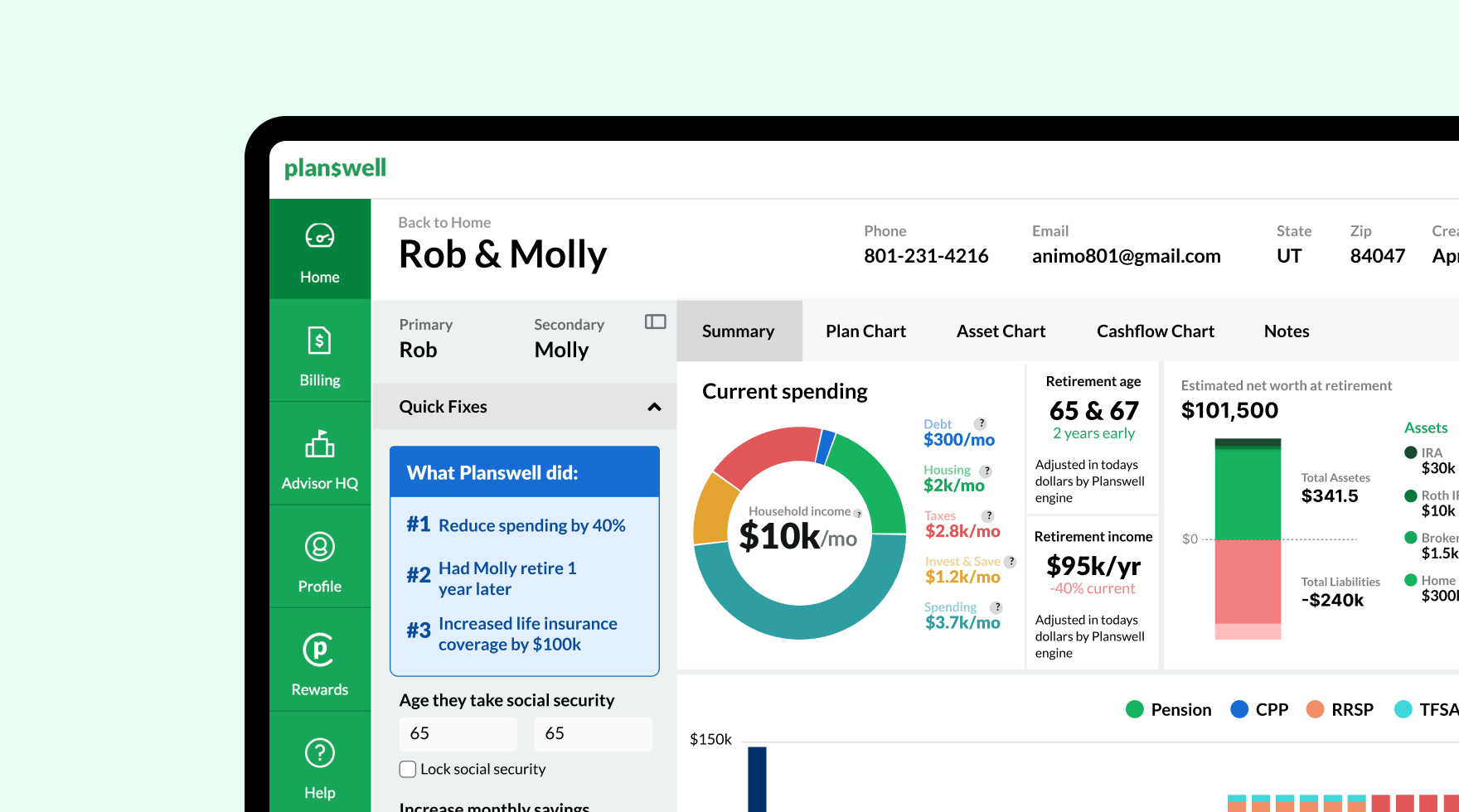

With Planswell, however, "you have a lot of information." At the very least, you know Planswell households "want some kind of clarity" about their retirement options. Plus they've taken the time to fill out our discovery survey and SMS validate their phone numbers, so you know they're "committed to finding out more" at the very least.

All of this information, Alex says, makes calling Planswell households "way better than a cold call." Plus, "the lead quality really surprised me," he notes.

Since he started with Planswell a year ago, Alex has noticed that most of our households fall into one of two main categories: first are folks who are 40+ and already have over 300k in AUM with solid incomes. The other are HENRYs: High Earners but Not Rich Yet. These younger people are making good incomes but haven't had the chance to start saving seriously yet.

Both are great clients to acquire.

At this point, Alex has $2 million in AUM and $30,000 in insurance premiums from Planswell households. "It's paid for itself indefinitely," he chuckles.

-1.png)

.png)